Why oil is one of the primary markets to price geopolitical risk and how investors and corporates could adapt

Executive Summary

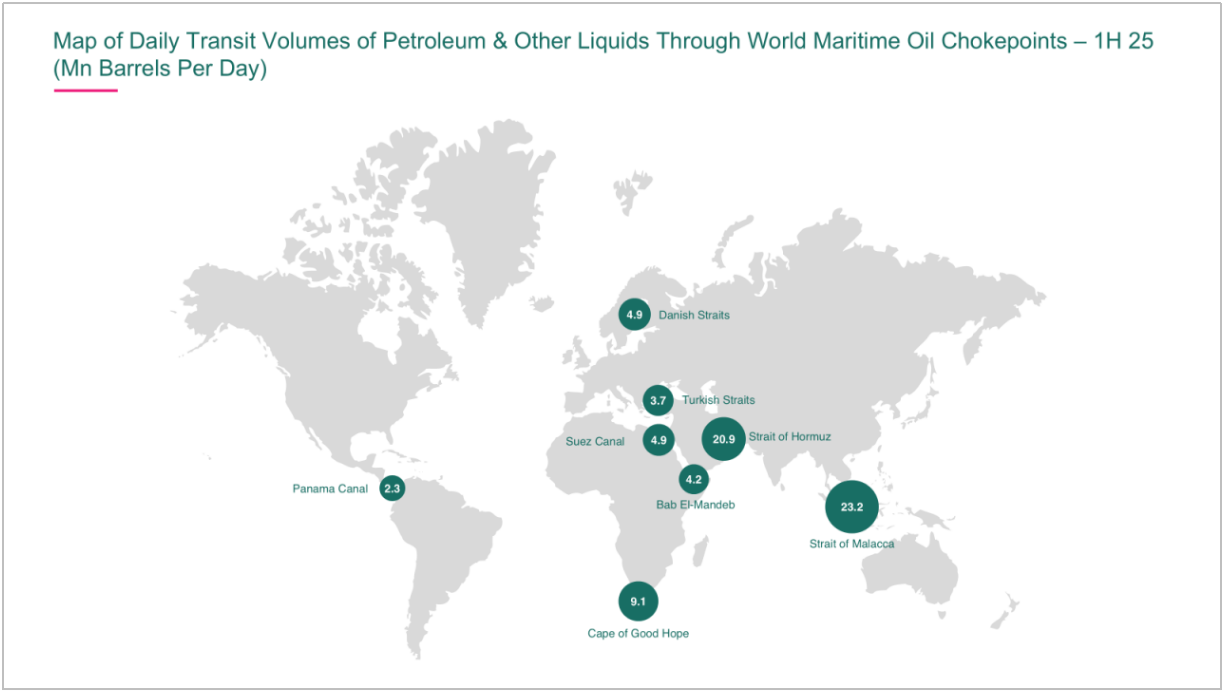

- Oil has become one of the market’s fastest geopolitical signals: around 79.7-80.2 million b/d of global maritime oil trade moves by sea, meaning even localized disruptions can reprice supply risk quickly, often ahead of broader risk assets.

- This responsiveness reflects oil’s unique structure (deep futures/options liquidity) and chokepoint concentration: Strait of Malacca ~22.5-24.0 million b/dand Strait of Hormuz ~20.7-21.8 million b/d are the two largest transit corridors, creating non-linear outcomes when buffers are thin.

- The system is structurally “tight” because large shares of seaborne oil move through a few constrained corridors. In 1H25, Strait of Malacca (23.2 million b/d)and Strait of Hormuz (20.9 million b/d) together represent ~42% of world maritime oil trade (79.8 million b/d)—a concentration that mechanically embeds a higher risk premium when geopolitical friction rises.

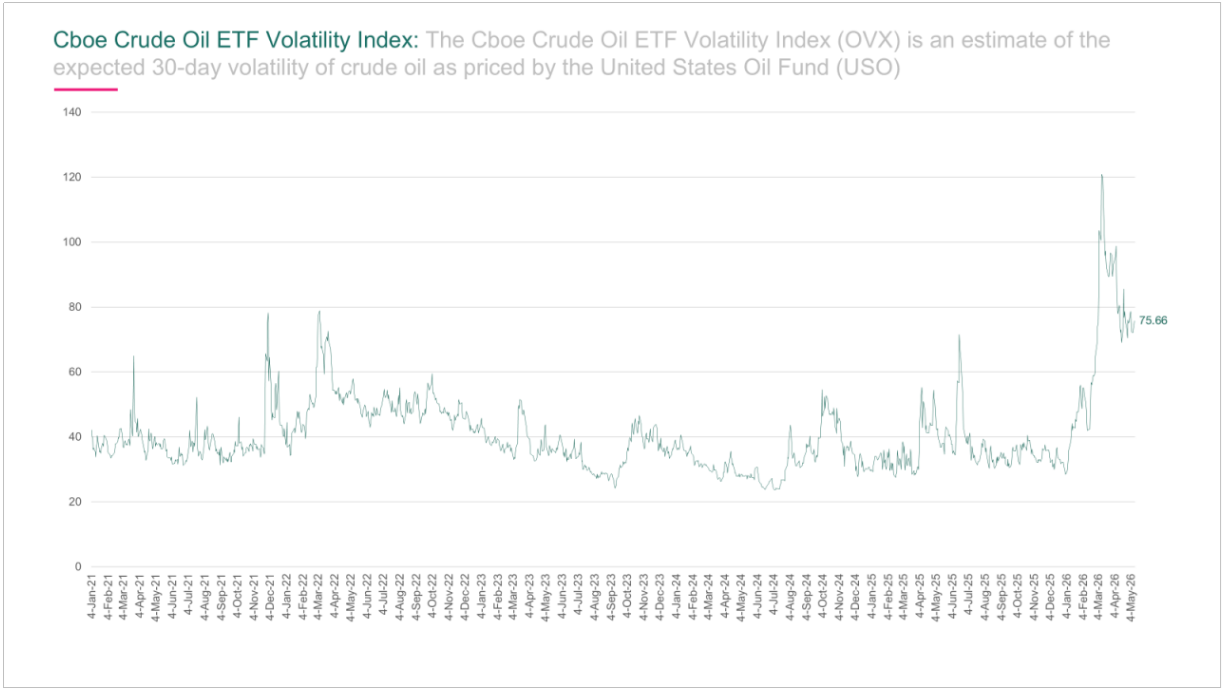

- Oil volatility transmits into asset pricing through inflation and policy rates, equity risk premia, FX, and credit. In periods of stress, crude volatility measures can spike materially (e.g., the Cboe Crude Oil ETF Volatility Index (OVX)has recently printed in the ~70 to 100+ range), reinforcing faster repricing of discount rates and risk premia across portfolios.

- A practical response requires scenario discipline and governance. Define 3-4oil scenarios (e.g., $65-$75, $75-$85, $95-$110, and $120+ Brent bands), translate them into cash-flow and discount-rate sensitivities, monitor leading indicators (freight, inventories, implied volatility), and pre-agree triggers for hedging, liquidity buffers, and capital allocation.

1. Oil Has Become the World’s Primary Geopolitical Risk Barometer

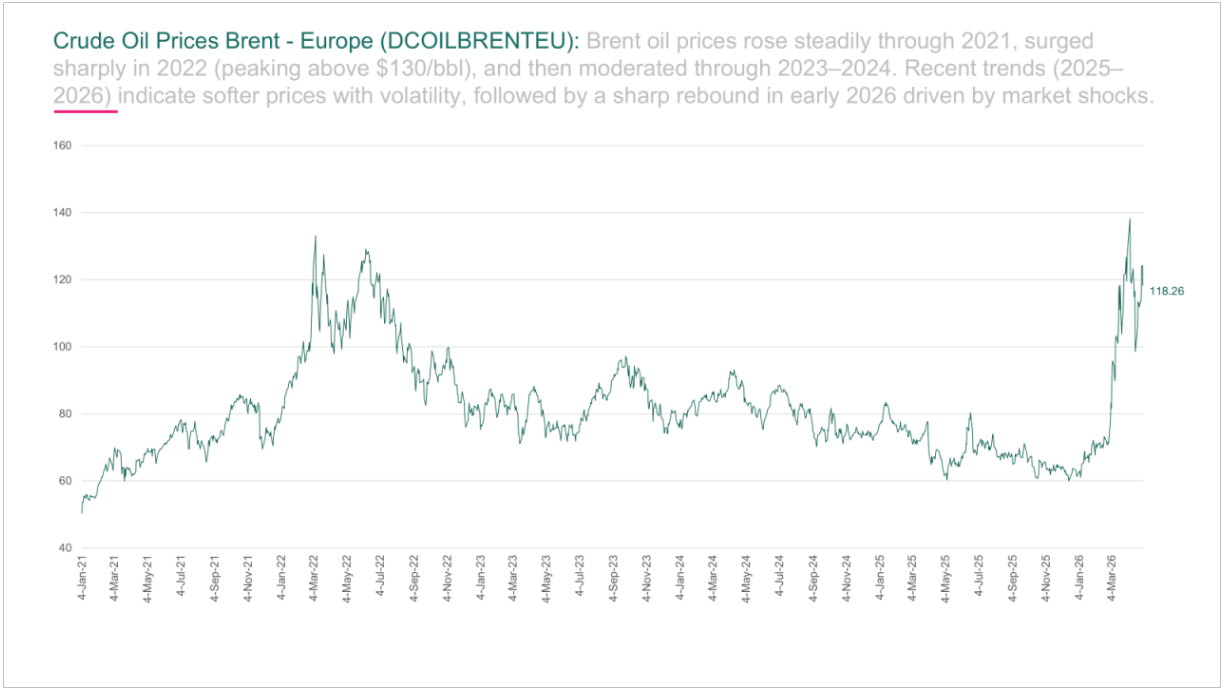

Oil prices used to be primarily driven by macro data and inventory cycles. Today, they often react first to geopolitical escalation-missile launches, drone strikes, shipping disruptions, and sudden shifts in diplomatic posture-frequently repricing risk before equities, rates, or FX.

Two features make oil a particularly sensitive barometer. First, it is highly liquid and continuously repriced across time zones, so information is incorporated quickly. Second, marginal changes in supply availability, especially around strategic chokepoints, have outsized effects on price when spare capacity is limited.

Source: U.S. Energy Information Administration (EIA). URL: https://fred.stlouisfed.org/series/DCOILBRENTEU

- Liquidity and Speed:Brent/WTI futures and options react immediately, while equities often wait for “risk sentiment” to consolidate.

- Chokepoint Math:Threats around the Strait of Hormuz, Suez/Red Sea, or key pipelines create non-linear outcomes because rerouting is costly and capacity is finite.

Volume of crude oil and petroleum liquids transported through world chokepoints and the Cape of Good Hope, 2020-1H25

| Location | 2020 | 2021 | 2022 | 2023 | 2024 | 1H25 |

|---|---|---|---|---|---|---|

| Strait of Malacca | 22.8 | 22.1 | 23.0 | 24.0 | 22.5 | 23.2 |

| Strait of Hormuz | 19.2 | 19.7 | 21.9 | 21.8 | 20.7 | 20.9 |

| Suez Canal and Sumed Pipeline | 5.4 | 5.2 | 7.3 | 8.8 | 4.8 | 4.9 |

| Bab El-Mandeb | 5.7 | 6.0 | 8.0 | 9.3 | 4.1 | 4.2 |

| Danish Straits | 3.1 | 3.1 | 4.2 | 5.0 | 4.9 | 4.9 |

| Turkish Straits (Dardanelles) | 3.2 | 3.3 | 3.2 | 3.5 | 3.6 | 3.7 |

| Panama Canal | 1.7 | 1.8 | 2.2 | 2.2 | 2.0 | 2.3 |

| Cape of Good Hope | 7.9 | 7.2 | 6.1 | 6.2 | 9.3 | 9.1 |

| World Maritime Oil Trade | 74.1 | 75.9 | 78.6 | 80.2 | 79.7 | 79.8 |

| World Total Oil Supply | 94.1 | 95.8 | 100.6 | 102.6 | 103.3 | 104.4 |

Source: U.S. Energy Information Administration (EIA) – “World Oil Transit Chokepoints”. URL:https://www.eia.gov/beta/international/regions-topics.php?RegionTopicID=WOTC

- Spare Capacity and Buffers:Lower effective spare capacity means each incremental disruption increases the probability of a shortage (and therefore a higher risk premium).

- Physical-to-Financial Feedback:Freight rates, insurance premium, and inventory behavior feed back into futures curves (backwardation/contango) and volatility.

- Policy Sensitivity:Strategic petroleum releases, sanctions, and OPEC+ decisions transmit directly into supply expectations.

- Conflict escalation (e.g., Iran-Israel) can trigger sharp intraday moves in Brent crude.

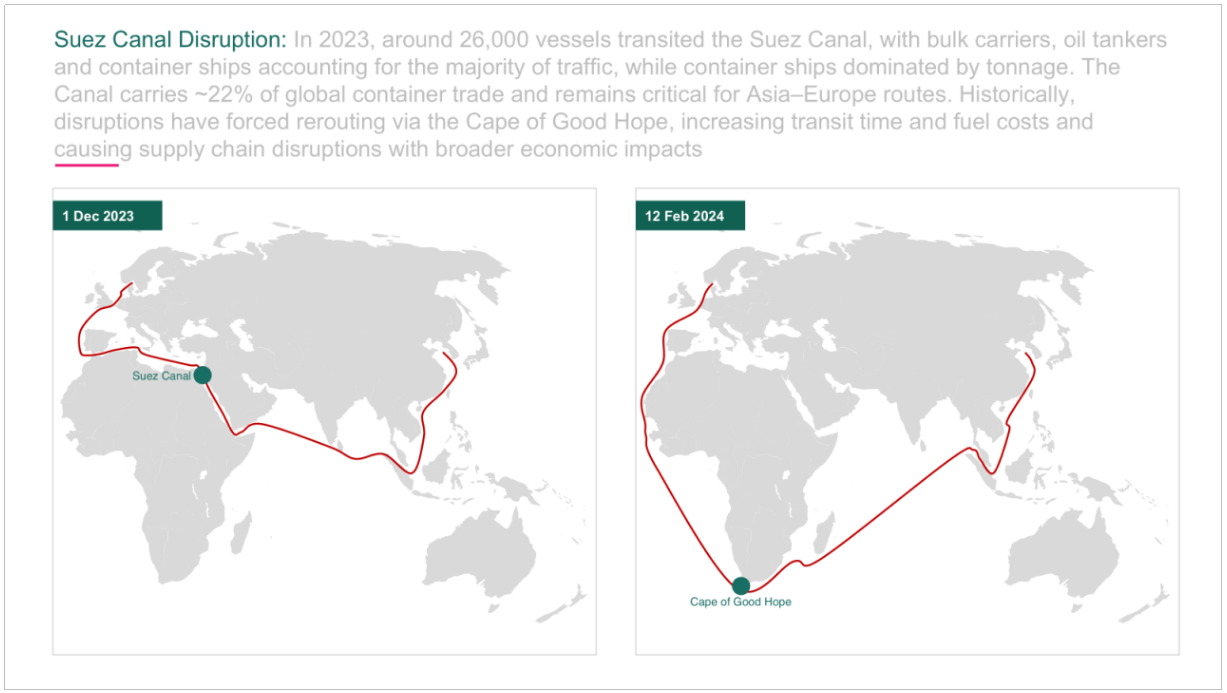

- Red Sea disruptions have rerouted shipping around Africa, extending transit times and increasing freight costs.

- OPEC+ supply cuts can amplify shocks by reducing spare capacity available to absorb disruptions.

2. Oil Volatility is Now Embedded in Global Asset Pricing

Traditional valuation frameworks (CAPM, WACC, DCF) often treat geopolitical shocks as short-lived. In practice, persistent oil volatility now influences core assumptions across asset classes—especially inflation expectations, terminal rates, and risk premia.

Source: Cboe Global Markets – “OVX Index Dashboard (Cboe Crude Oil ETF Volatility Index)”.

URL: https://www.cboe.com/us/indices/dashboard/ovx/ (Accessed: 12 May 2026).

2.1 Equities: Higher Oil Volatility Can Widen the Equity Risk Premium

In equities, oil volatility matters less as a one-off cost shock and more as a driver of uncertainty around inflation, margins, and policy. That uncertainty typically lifts required returns (ERP) and compresses valuation multiples, especially for long-duration growth and fuel-sensitive sectors.

- Transmission:Higher oil prices can lift inflation expectations. This often keeps policy rates tighter for longer, increases discount rates, and contributes to a wider equity risk premium.

- Most Impacted:Consumer discretionary, aviation, logistics, and energy-intensive manufacturing; emerging markets with large net import bills.

- Relative Beneficiaries:Energy producers and select midstream/LNG-linked businesses through stronger near-term cash flows and improved earnings visibility.

Public Equity

Public markets tend to reprice oil risk quickly via sector rotation, factor moves (value vs growth), and changes in inflation/rates expectations that feed directly into equity discount rates and multiples.

- Multiples and Duration:Higher real rates typically compress long-duration growth stocks more than near-cash-flow value stocks.

- Earnings Dispersion:Margin pressure concentrates in transport, chemicals, consumer, and industrials without pass-through; energy and select commodities benefit.

- Index/Flow Effects:Risk-off episodes can drive broad de-risking and correlation spikes, reducing diversification benefits in the short run.

- EM Sensitivity:Net oil importers can see faster equity drawdowns due to FX/inflation pass-through and tighter domestic financial conditions.

Private Equity

In private equity, oil volatility transmits more through financing conditions and exit markets than through immediate mark-to-market moves. The key impact is on leverage capacity, debt pricing, and the multiple investors are willing to pay for cyclical or cost-exposed earnings.

- Leverage and DSCR Headroom:Higher base rates and wider spreads reduce sustainable leverage and raise equity checks, especially for operationally heavy businesses.

- Cash Flow Quality Focus:Investors pay more for contracted revenue, indexation, and pricing power; they discount businesses with fuel/utility exposure and weak pass-through.

- Exit Multiple Risk:IPO windows and strategic M&A appetite can shut during oil-driven risk-off periods, extending holding periods and lowering realized MOIC/IRR.

- Underwriting Discipline:Scenario-based budgeting (oil at $65/$80/$100+) becomes essential for covenant sizing, working capital, and capex pacing.

Venture Capital

VC is typically the most rate-sensitive segment because value is concentrated in long-dated outcomes. Oil-driven inflation volatility can push up discount rates and reduce risk appetite, which tightens funding and raises the bar for “path-to-profitability.”

- Valuation Reset Risk:Higher discount rates reduce forward revenue multiples; down-round frequency rises as comparables reset.

- Funding Availability:LP risk budgets tighten and fundraising slows; runway planning and burn discipline become primary diligence items.

- Exit Pathways:Weaker IPO markets push startups toward secondary sales, structured rounds, or strategic exits at lower headline multiples.

- Winners in Volatility:Energy efficiency, logistics optimization, and risk/insurance tech can see demand uplift as corporates prioritize resilience.

2.2 Fixed Income: Rates, Credit Spreads, and Liquidity

Rates (Yield Curve and Duration)

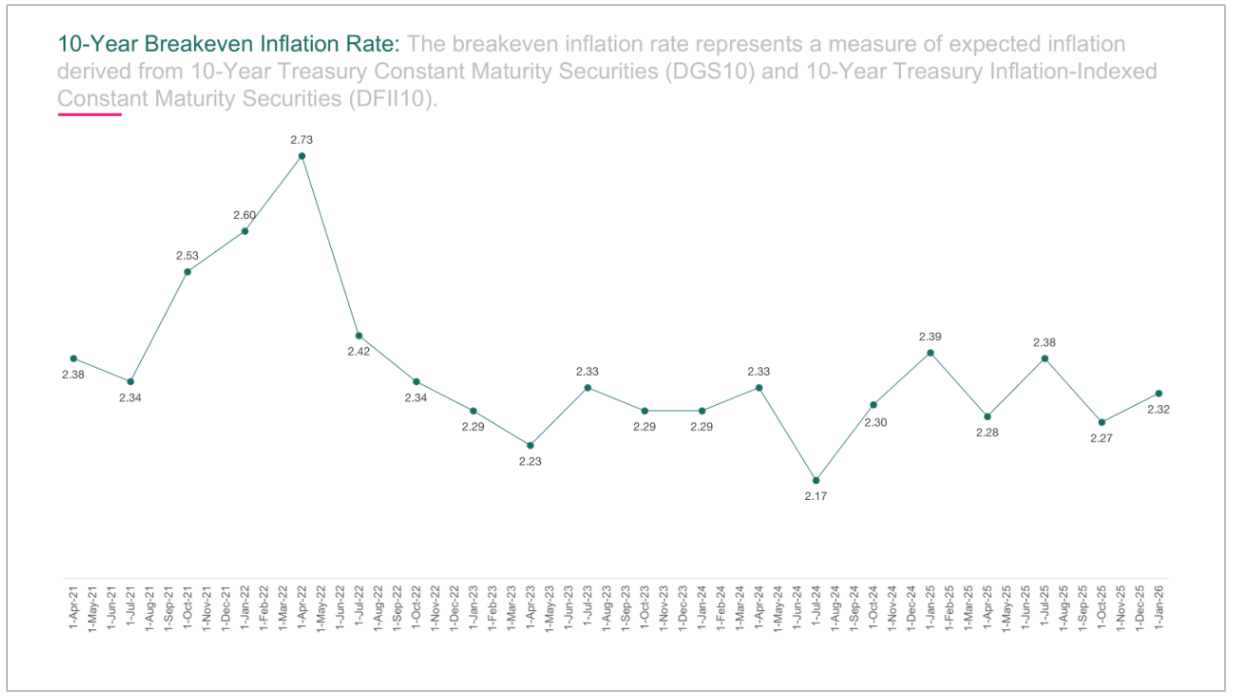

A geopolitical-driven oil shock can create a mixed rates response—front-end yields may rise on inflation concerns, while longer-dated yields can fall on risk-off positioning. The net effect depends on whether markets treat the shock as inflationary (higher term premium) or growth-negative (flight to quality), and whether central banks can credibly “look through” energy-driven inflation.

- Higher inflation risk can lift short-term yields and delay expected rate cuts.

- Risk aversion can increase demand for duration, compressing long-end yields.

- Result: curve shifts (flattening or bull steepening) and a higher term premium in volatile periods.

Source: Federal Reserve Bank of St. Louis (FRED) – “10-Year Breakeven Inflation Rate (T10YIE)”.

URL: https://fred.stlouisfed.org/series/T10YIE (Accessed: 12 May 2026).

Credit and Liquidity (Spreads and Funding)

Beyond the risk-free curve, oil volatility can widen credit spreads and lift liquidity premia as markets reprice growth and margin risk. This is typically most visible in higher all-in yields, weaker primary issuance windows, and a sharper differentiation between resilient balance sheets and cyclical cash flows.

Sovereigns & Rates

For sovereign curves, the market impact hinges on whether oil is viewed as inflationary (pushing yields higher) or recessionary (driving flight-to-quality into duration). Oil-importers typically face a more adverse inflation-growth mix than exporters.

- Curve Dynamics:Front-end reprices policy expectations quickly; long-end reflects growth/risk sentiment and term premium.

- Breakeven:Energy shocks can lift inflation breakeven even if real growth expectations soften.

- Exporters vs Importers:Exporters may see improved fiscal buffers (spread support), while importers can face deteriorating external balances (spread pressure).

Investment Grade Credit

In IG, the first-order move is usually wider spreads from uncertainty and sector dispersion, plus higher all-in yields from rates. Balance-sheet strength and pricing power become more important differentiators when energy costs are volatile.

- Sector Dispersion:Transport, chemicals, airlines, and heavy manufacturing can see widening faster spread versus defensives.

- All-in Yield:Even if spreads are stable, higher rates raise refinancing cost and can weaken interest coverage at the margin.

- Liquidity Premium:During risk-off, bid-ask spreads widen and issuance windows can temporarily close, increasing new-issue concessions.

High Yield & Leveraged Loans

High yield and loans are more sensitive because they sit closer to the default boundary. Higher fuel and input costs can hit EBITDA quickly, while higher base rates increase cash interest. This combination can stress covenants and reduce recoveries in downside cases.

- Coverage and DSCR Stress:Higher rates plus weaker margins reduce interest coverage and debt service metrics, especially for floating-rate structures.

- Refinancing Walls:Volatility can shut issuance windows; maturities become a catalyst for distressed exchanges or equity injections.

- Winners/Losers:Issuers with strong pass-through and contracted revenue hold up; fuel-intensive, low-margin businesses see faster spread blowouts.

2.3 FX: Energy Risk Is Being Repriced

Energy price shocks tend to weaken oil-importer currencies and support exporter currencies, shaping hedging costs, earnings translation, capital flows, and sovereign borrowing conditions. In sustained spikes, the balance-of-payments impact (wider current account deficits for importers) can become as important as interest-rate differentials in driving FX moves.

- Importers:Pressure on INR, JPY, and EUR during sustained oil spikes due to higher trade deficits and inflation passthrough.

- Exporters:Relative support for SAR/AED-pegged regimes (via fiscal buffers) and for floating exporters such as CAD.

- Corporations:Higher hedging costs and greater volatility in USD-reported earnings for firms with unhedged energy exposure.

2.4 Real Estate: Cap Rates, Financing Costs, and Operating Expenses

Real estate is affected through the same discount-rate mechanism as other long-duration assets, but with additional sensitivity to debt availability, cap rate expansion, and energy-linked operating costs (utilities, maintenance, and construction inputs).

- Cap Rates:Higher risk-free rates and risk premia can expand cap rates, lowering asset values unless NOI growth offsets.

- Financing and DSCR:Higher all-in borrowing costs reduce proceeds and tighten DSCR sizing; refinance risk rises for floating-rate borrowers.

- Operating and Build Costs:Utilities and service charges can rise; construction materials and logistics costs can pressure feasibility and delay projects.

3. Why This Volatility Regime Looks Structural (Not Cyclical)

Oil volatility is increasingly driven by repeatable structural forces rather than isolated events. Four dynamics stand out:

-

Multipolar Geopolitics:

Multiple simultaneous flashpoints (Middle East, Russia-Ukraine, and broader great-power competition) raise the frequency of risk events.

-

Weaponization of Trade Routes:

Chokepoints such as the Red Sea route, Strait of Hormuz, and Suez Canal are strategic levers, not just logistics corridors.

Source: UNCTAD – “Navigating troubled waters: Impact to global trade of disruption of shipping routes in the Red Sea, Black Sea and Panama Canal” (Rapid Assessment, Feb 2024).

URL: https://unctad.org/system/files/official-document/osginf2024d2_en.pdf (Accessed: 12 May 2026).

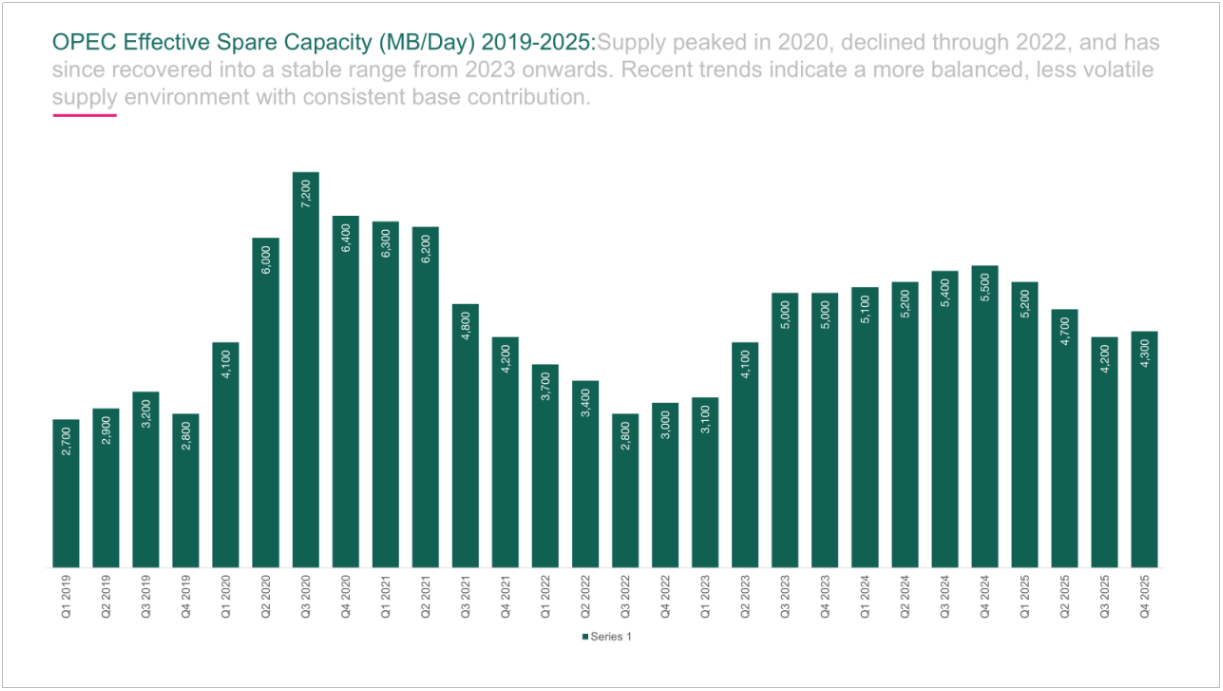

OPEC+ as a Volatility Amplifier: Supply discipline can reduce buffers and increase the sensitivity of prices to geopolitical headlines.

Source: International Energy Agency (IEA) – “OPEC effective spare capacity, 2019-2025”

URL: https://www.iea.org/data-and-statistics/charts/opec-effective-spare-capacity-2019-2025

An additional driver is the uneven investment cycle created by the energy transition. While long-term policy aims to reduce fossil fuel dependence, near- and medium-term demand remains resilient. If upstream investment and maintenance lag demand, the system operates with tighter buffers—making prices and volatility more sensitive to geopolitical headlines and weather-related disruptions.

4. Scenario Analysis: How Oil Prices Could Move Markets

| Scenario | Brent (illustrative) | Market Implications (Key Transmission) |

|---|---|---|

| De-escalation/Demand Slowdown | ~$65-$75 | Disinflation impulse; rate-cut expectations improve; equity multiples stabilize/expand; credit spreads tighten; oil exporters see softer fiscal tailwinds and moderating liquidity support. |

| Base Case (Contained Volatility) | ~$75-$85 | Inflation broadly contained; central banks cautious but stable; equity style rotation limited; EM FX mostly range-bound; carry strategies remain viable with selective risk management. |

| Moderate Escalation (Regional Disruption) | ~$95-$110 | Higher inflation risk and term premium; front-end yields pressured; equity risk premium widens; fuel-sensitive sectors underperform; USD strengthens; oil-importer FX weakens; credit spreads widen modestly with weaker liquidity. |

| Severe Disruption (Chokepoint Shock) | $120+ | Acute inflation spike with growth downside; policy constraints rise (cuts delayed or hikes risked); equities correct and correlations rise; flight-to-quality into USD and gold; EM stress increases; HY spreads gap wider and primary markets can shut temporarily. |

| Note: Brent levels are illustrative ranges for scenario framing (not forecasts). Market impacts reflect typical first- and second-order transmission via inflation expectations, policy rates, risk premia, FX, and credit liquidity. | ||

5. Implications for Corporate Finance and Valuation

5.1 Higher WACC and Lower DCF Values

Higher oil prices can raise inflation expectations and policy rates, increasing the cost of debt and the cost of equity. The combined effect raises WACC and compresses DCF-based valuations (including real estate feasibility and leveraged project returns).

- Finance Teams:Separate base-case budgeting from risk scenarios; quantify WACC sensitivity to oil-driven inflation and credit spreads.

- Treasury:Review hedging policy (fuel, FX, and interest rates) and align hedge horizons with procurement cycles and debt reset dates.

- Commercial:Embed pass-through clauses, fuel surcharges, or indexation where feasible; renegotiate contract tenors to reduce exposure.

- Capital Allocation:Stage capex and preserve liquidity buffers; ensure covenant headroom reflects downside oil scenarios rather than only historical averages.

5.2 Margin and Cash Flow Pressure in Energy-Intensive Sectors

Oil-driven cost inflation typically hits cash flow through both direct energy inputs and second-order effects across supply chains. The severity depends on contract structure (ability to pass through costs), the timing mismatch between cost increases and price resets, and how much working capital the business must carry to operate.

- Direct energy inputs (fuel, diesel, electricity, and gas) can compress gross margin immediately where costs are not indexed or hedged.

- Second-order input inflation can follow as suppliers reprice logistics, packaging, chemicals, metals, and other oil-linked feedstocks, widening the cost base beyond energy lines.

- Operating cost pressure often extends to contractors and services, because higher fuel costs raise on-site mobility, maintenance, and outsourced transport rates.

- Working capital requirements can increase when companies carry higher-value inventories, pre-buy fuel or critical inputs for continuity, or face slower receivable collections in stressed customer segments.

- Demand elasticity can amplify cash flow risk, as end-customers reduce volumes or trade down when fuel-driven inflation hits disposable income and freight surcharges increase delivered prices.

- Mitigation typically combines pricing and contract tools (indexation, pass-through clauses, and shorter reset cycles) with operational levers such as route optimization, energy efficiency capex, selective hedging, and tighter credit control.

5.3 Refinancing Risk and Covenant Sensitivity

- Floating-rate borrowers face higher interest expense and weaker debt service metrics (e.g., DSCR).

- Higher volatility can tighten credit spreads and reduce lender appetite for cyclical or energy-sensitive exposures.

- Refinancing planning should incorporate higher-for-longer base rates and downside oil scenarios.

7. What Investors Should Do

- Explicitly Price A Geopolitical Risk Premium:Reflect oil volatility, supply-chain risk, and FX instability in scenario assumptions (not only in narrative). Translate this into explicit inputs such as higher volatility bands, wider discount-rate ranges, and more conservative terminal assumptions for high-risk exposures.

- Use Natural Hedges:Consider energy producers, LNG-linked names, and midstream infrastructure as partial hedges to geopolitically driven price shocks. Size these positions with an explicit objective, such as protecting portfolio cash flow or reducing drawdowns during risk-off episodes.

- Stress-Test For $100-$120 Oil:Especially for airlines, autos, chemicals, logistics, and EM equities with high import dependence. The test should include second-order effects such as freight inflation, weaker consumer demand, and tighter funding conditions.

- Define Trigger-Based Actions:Pre-define what you will do if oil volatility breaches a threshold, such as increasing hedges, reducing leverage, rotating factor exposure, or raising liquidity. This reduces decision lag when headlines move faster than committee cycles.

- Focus On Balance Sheet & Funding Resilience:Prefer businesses and credits with strong interest coverage, flexible cost structures, and pricing power. For private assets, underwrite refinance risk explicitly, including higher spreads and slower exit markets.

- Selective Allocation to Commodity-Linked Markets (Including GCC):Focus on balance-sheet strength, policy buffers, and cash-flow resilience. Evaluate how fiscal buffers, sovereign liquidity, and domestic credit conditions change under both higher and lower oil scenarios.

8. Bottom Line

The global economy has entered a regime where geopolitics can dominate oil price action—and oil, in turn, transmits that risk into equities, rates, FX, and corporate valuation. For analysts and decision-makers, the practical response is clear: treat oil as a macro risk factor, embed it into scenarios, and reflect its impact through discount rates, cash-flow stress tests, and portfolio construction.

Practical Checklist: Start by defining three to four oil scenarios that include both spikes and drawdowns, and specify the time horizon for each scenario. Translate each scenario into financial drivers by adjusting revenue and margin assumptions, working capital needs, and funding costs in a consistent way. Update valuation inputs by reflecting the scenario impact on discount rates, risk premia, and exit multiples, and ensure the assumptions are internally consistent with the macro narrative. Finally, agree the playbook in advance by defining hedges, pricing actions, capex pacing, and liquidity or covenant buffers that are triggered when scenario thresholds are reached.

In this environment, the objective is not to forecast a single oil price, but to reduce surprise by making exposures visible and decisions repeatable. Portfolios that combine scenario discipline with liquidity management and selective hedges are better positioned to navigate regimes where geopolitical headlines can reprice risk faster than fundamentals can adjust.

Leave a Reply