Introduction

Saudi Arabia’s real estate market has traditionally been dominated by public sector investments. However, the growing need for efficiency, innovation, and shared financial responsibility has led to the rise of Public-Private Partnerships (PPPs), redefining the landscape of real estate investment and development.

A Public-Private Partnership (PPP) is a collaborative long-term contractual agreement between government institutions and private sector organizations to develop, finance, operate, and maintain public infrastructure or deliver essential services, combining public oversight with private sector efficiency for optimal public benefit. By pooling resources, expertise, and risk, PPPs have become a transformative force in large-scale infrastructure and real estate developments, helping government meet the growing demands for urban expansion, affordable housing, and commercial real estate.

Over the past few years, especially as the country navigates through its ambitious Vision 2030 Strategy, sectors such as construction, power, and transportation have attracted significant PPP investments. Major projects like the King Abdullah Financial District, the Red Sea Development, affordable housing projects under the ‘Sakani’ initiative, among other ‘giga’ projects showcase that PPPs are emerging as a pivotal mechanism in revolutionising the real estate landscape, driving economic diversification, and creating unprecedented opportunities for sustainable development.

The Evolution of PPP Landscape

In the Kingdom of Saudi Arabia, the adoption of PPP models has significantly increased in recent years, especially driven by the government’s commitment to accelerate economic diversification and infrastructure modernization under Vision 2030. However, PPPs have a long-standing history.

The public-private partnerships trace their roots to ancient infrastructure projects, but their modern form emerged in 1980s Europe before spreading globally. In the Gulf region, the United Arab Emirates became the early adopter of PPP models in the late 1990s, particularly for utilities and transport projects, while other Gulf nations like Qatar and Oman developed their own models for energy and infrastructure projects. Across the region, PPPs have become instrumental in economic diversification efforts, combining Islamic finance structures with international best practices.

Saudi Arabia’s journey toward privatization commenced in 1997 with the approval of the Privatization Strategy, a pivotal move aimed at bolstering private sector participation in the national economy. This strategic initiative laid the foundation for comprehensive institutional and legal reforms across 20 key sectors, necessitating the development of dedicated regulatory frameworks and the establishment of specialized institutional structures. By fostering a more dynamic and competitive economic environment, the Kingdom positioned itself to leverage private sector expertise and investment for sustainable growth. This step was substantiated by establishment of ‘The National Center for Privatization & PPP (NCP)’ in 2017. The center oversees privatization and PPP initiatives, collaborating with ministries to identify projects, standardize procedures, and enforce regulations. It ensures alignment with Vision 2030, with policy support from the Council of Economic and Development Affairs (CEDA). Over the years, the NCP has approved a pipeline of 200 PPP projects, spanning 17 key sectors, with total investments surpassing $50 billion.

In 2021, the Private Sector Participation (PSP) Law, The Kingdom Of Saudi Arabia’s first comprehensive PPP legislation, marked a major milestone, enabling greater private investment and driving economic transformation. The PSP law allows arbitration, ensures equal treatment of local and foreign investors, and offers flexibility in Saudization for specialized projects.

The current PPP framework in place is backed by strong governance, clear policies, and a growing project pipeline. By actively courting investors and publishing project roadmaps, the Kingdom has extensively leveraged private-sector expertise in national development.

Decoding the PPP Framework

A PPP represents a symbiotic relationship where the private sector provides capital, expertise, and operational efficiency while the government ensures regulatory compliance and project sustainability.

In essence, several stakeholders play a key role when defining the PPP framework. The Real Estate PPP ecosystem, particularly, encompasses a diverse range of entities, each playing a crucial role in shaping the sector’s growth and development. Private developers and consortiums contribute technical knowledge and financial backing, while financial institutions help structure investment models and mitigate risks. Real estate investment companies manage assets and optimize project returns, ensuring profitability for investors. International partners and consultants provide regulatory guidance, while government and regulatory bodies streamline approval processes and maintain legal oversight. The Public Investment Fund (PIF) also plays a critical role by financing large-scale projects and reducing investment risks, thereby encouraging foreign and domestic participation.

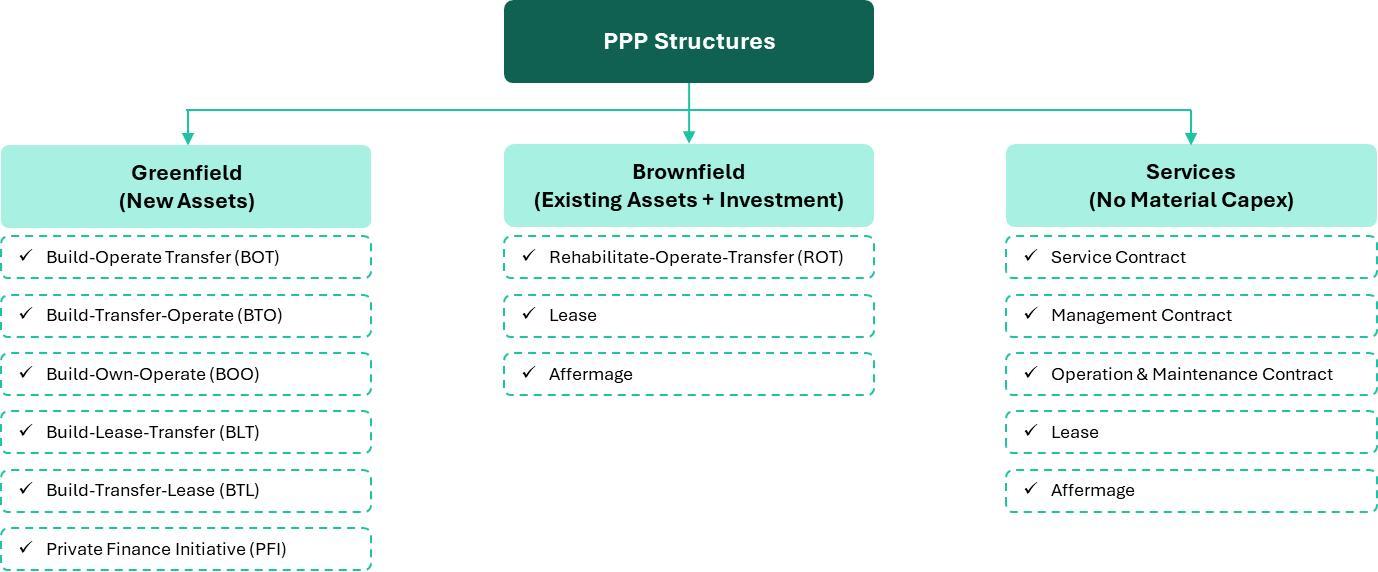

Subsequently, varying interaction models can lead to different structures of PPP, depicting degrees of private sector involvement in project development, ownership, and operation. These models range from minimal private sector participation, where the government retains substantial control, to fully privatized arrangements where the private sector assumes significant responsibilities. The flowchart below outlines key PPP models, showcasing their distinct frameworks and responsibilities:

However, emerging PPP trends in Saudi Arabia reflect a shift towards hybrid models to attract investment while ensuring long-term sustainability.

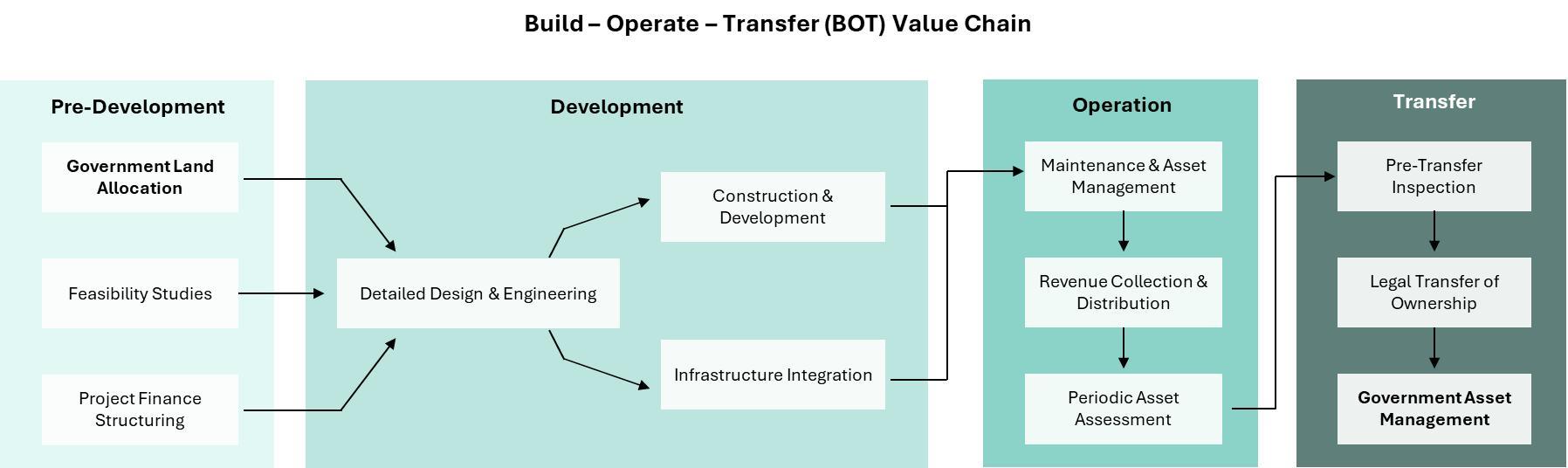

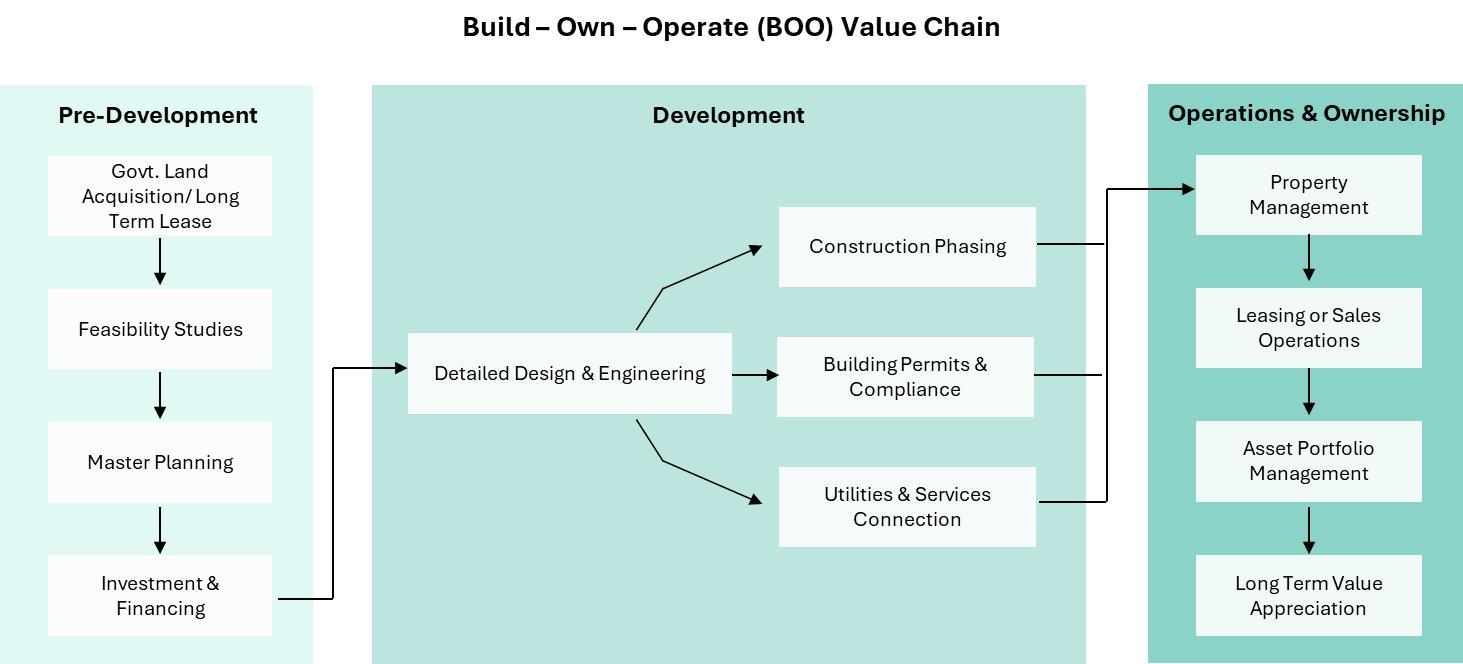

Specifically, within the Saudi real estate sector, models like Build-Operate-Transfer (BOT) and Build-Own-Operate (BOO) have proven particularly effective, combining private sector efficiency with mechanisms to mitigate financial risk.

In the Build-Operate-Transfer (BOT) Model, the private sector builds and operates the project for a set period before transferring ownership to the government. These projects are normally large-scale, greenfield infrastructure projects that would otherwise be financed, built, and operated solely by the government.

Whereas, in a Build-Own-Operate (BOO) Model, the private entity finances, builds, owns, and operates the project indefinitely, with regulatory oversight. This model is ideal for large, complex PPP infrastructure projects, particularly high-value ventures requiring specialized operational expertise.

Such PPP Models lead to value creation by optimally distributing risks between public and private sectors, accelerating project delivery timelines by 20-30%, while bringing international expertise to enhance quality standards as compared to traditional procurement methods. These partnerships further enable fiscal flexibility by reducing immediate capital requirements for the government, effectively supporting ambitious development goals.

Current Scenario of PPP Investments in Saudi Real Estate

Saudi Arabia’s real estate sector has doubled its contributions to the country’s economy from 5.9% in 2023 to around 12% in 2024. This surge has been supported by new legislation streamlining regulations, including over 20 new regulations that aim to facilitate development and boost investor confidence. The shift represents a strategic approach to accelerating development, optimizing resource allocation, and attracting foreign and domestic investments.

In the Kingdom Of Saudi Arabia, PPPs have expanded significantly, rising from 3.5% of total government project value in 2018 to an average of 15.6% between 2019-2022. By 2023, PPP concession contracts hit a record $28.2 billion (representing 23% of total contracts awarded), before slightly declining to 18.3% in 2024, still above historical averages. In real estate, The Kingdom Of Saudi Arabia had 18 PPP projects in 2018, and by 2024, 192 project licenses were issued, totalling $39 billion.

Some of the successful real estate projects that leveraged PPP in the Kingdom Of Saudi Arabia, such as the Diriyah Development Project, the Riyadh Integrated Bus Network and the Shuqaiq 3 Independent Water Plant, underscores the pivotal role of well-structured financing, strategic partnerships and government backing in long-term project viability. Projects like the Jeddah Airport Expansion and Al-Faisaliah Hospital demonstrate that government commitment and international collaboration have driven successful execution. Furthermore, the Diriyah Joint Venture model illustrates that heritage-based developments attract substantial foreign investment when combined with transparent governance and cultural integration. Ultimately, the success of these projects underscores the value of strong government backing, clear regulatory frameworks, and international collaboration in achieving financial, social, and environmental goals over time.

PPP Models Across GCC Real Estate: Differentiation Through Strategic Specialisation

The GCC’s real estate PPP sector has evolved into a dynamic competitive arena where each nation’s model reflects deliberate and unique strategic positioning. The UAE has established itself as the innovation leader through its emirate-level flexibility, with Dubai’s performance-linked PPP contracts achieving 22% faster project delivery than regional averages, while Abu Dhabi’s REIT integrated models offer superior liquidity options for institutional investors. Qatar has carved out a niche in legacy asset optimization, converting 92% of FIFA facilities into revenue-generating public assets through its unique modular tournament-based PPP framework. Saudi Arabia dominates in scale and systemic efficiency, with its NCP’s standardized documentation reducing procurement timelines by 40% compared to neighbouring markets, all while maintaining Sharia-compliance through Mudaraba and Musharaka financing, however, this comes with stricter local content requirements that increase costs by 15-20%. Oman and Bahrain have adopted a focused differentiation strategy. Oman’s mid-market tourism PPPs deliver 18% higher return on investments for regional investors through optimized risk-sharing structures, while Bahrain’s fintech-enabled contracts reduce transaction costs by 30% through smart contract automation. Kuwait, on the other hand, represents the most investor-friendly regime, with its tradable PPP securities and 10-year tax holidays creating a secondary market that has grown 47% since 2021, annually.

What makes the GCC particularly formidable is how these competing models also create complementary strengths: Saudi’s scale enables giga-projects, while the UAE’s flexibility fosters innovation; whereas Qatar specializes in asset repurposing, where Oman focuses on sustainable mid-market yields. This competitive diversity, combined with converging standards in digital monitoring (adopted by 78% of major projects) and green financing, positions the region as both a laboratory of partnership approaches and battleground for next generation PPP innovation, with each nation’s distinctive approach contributing to a robust regional ecosystem that collectively outperforms other emerging markets in project delivery efficiency by 35%. The PPP evolution is notably reflected by the region’s $214 billion pipeline, positioning GCC as a global leader in adaptable PPP frameworks.

The Growing Need for PPPs in The Kingdom Of Saudi Arabia: Why Now?

The Kingdom Of Saudi Arabia’s growing focus on PPPs is largely a response to declining government revenues caused by lower oil prices. With limited public funding available, PPPs offer a valuable solution by leveraging private sector investment to support major real estate projects.

The goal of The Kingdom Of Saudi Arabia’s Vision 2030 is to boost private-sector participation from 40% to 65% of GDP by 2030, positioning PPPs as a crucial mechanism to drive this transformation, facilitating investment across vital sectors such as housing, transportation, energy, water, waste management, education, and healthcare. With rising demand and persistent shortages in these crucial sectors, the government’s shift toward PPPs is a strategic and necessary move. The expanding private-sector involvement can help bridge gaps, accelerate development, and enhance service quality, ensuring sustainable growth for the economy. Central to this effort, the Public Investment Fund (PIF) has played a crucial role by injecting capital into strategic industries, attracting foreign direct investment (FDI), ultimately fostering PPP.

Critical Success Factors and Risk Mitigation Strategies

While PPPs have gained prominence quickly, few PPP projects in the Kingdom Of Saudi Arabia’s real estate sector have faced significant challenges that have led to delays and halted progress. These challenges highlight critical lessons on the importance of clear project structuring, financial planning, and realistic expectations. The Build-Operate-Transfer (BOT) and Build-Own-Operate (BOO) models too, while commonly used, have shown mixed results due to issues such as regulatory delays, labour disputes and overambitious scopes. Large-scale giga-projects, with their enormous budgets, exemplify the danger of overambitious timelines and financial overruns, while some projects have suffered from financial constraints and management turnover.

In Saudi Arabia’s real estate market, the success of PPPs hinges on a delicate balance of factors often overlooked in traditional analysis. Government commitment to transparent procurement processes and contract standardization has proven decisive, yet the most successful projects share a common thread: early stakeholder alignment on risk allocation before financial structuring begins. The overlooked barriers threatening project viability include capacity gaps within government entities to effectively monitor complex performance metrics and underdeveloped secondary markets for PPP refinancing—both potentially more damaging than frequently cited regulatory concerns.

Despite being instrumental in driving infrastructure development, PPPs are often fraught with significant risks which could hinder their success. One of the major challenges lies in financing and investment, particularly when projects lack clear and robust revenue models. Without predictable financial structures, investors may view these ventures as non-viable, reducing their appeal and delaying critical projects. For instance, the privatization of healthcare facilities under an insurance-based model faced limited private sector interest due to uncertainty in revenue streams. Additionally, risk allocation between the public and private sectors remains a contentious issue. Private operators are sometimes expected to assume considerable demand risk without adequate guarantees, discouraging participation and affecting project timelines.

Forward-thinking developers are mitigating these challenges through innovative approaches, including creating dedicated knowledge transfer programs within project structures and forming specialized joint ventures between international and local firms that blend global expertise with cultural intelligence. The projects demonstrating the greatest resilience have established formal governance mechanisms that adapt contract terms dynamically as market conditions evolve, suggesting that PPP success in the Kingdom ultimately depends less on initial deal structuring than on building institutional frameworks capable of managing long-term partnerships through market cycles.

Way Forward

To maximize the potential of PPPs in Saudi Arabia, building institutional capacity is paramount. A coordinated effort to enhance specialized expertise across public institutions will ensure more efficient project evaluation, structuring, and management. Establishing centers of excellence (COEs) dedicated to leveraging best PPP practices can significantly improve implementation outcomes. Additionally, evolving the contractual frameworks is essential, as rigid agreements often fail to accommodate changing market conditions, technological advancements, or shifting social priorities. The next generation of PPP contracts should emphasize flexibility, incorporating adaptive mechanisms and performance-based outcomes rather than prescriptive methods, thereby fostering innovation and efficiency. Equally important is optimizing risk allocation by developing sophisticated assessment methodologies to ensure that each risk is managed by the party best equipped to do so, ultimately reducing costs and expediting project timelines.

Financial innovation also plays a critical role. Beyond conventional funding models, leveraging green bonds—debt securities where proceeds are exclusively applied to eligible environmental projects, providing investors with both financial returns and positive environmental impact; social impact investments, and infrastructure funds can be vital in mobilizing capital. The Red Sea Development Company exemplifies this approach, having raised $3.76 billion through its landmark green financing facility in 2021, the largest in the Middle East to date. Similarly, ACWA Power’s Sudair Solar PV project has attracted over $900 million in social impact investments to deliver 70% of the country’s renewable energy under the National Renewable Energy Program (NREP). In addition, the Public Investment Fund (PIF) raised $5.5 billion in second green bond sale to fund renewable energy, sustainable water management, green buildings, and other eco-friendly projects under its Green Finance Framework. This carves a unique opportunity for the Saudi financial sector to create tailored financial vehicles that meet both investor expectations while aligning with the Kingdom’s development goals.

Conclusion

The path forward for PPPs in Saudi Arabia’s real estate sector is not merely about constructing buildings and infrastructure, but also about constructing a new economic and social reality. By embracing innovation, sustainability, and inclusive growth principles, these partnerships will serve as catalyst for the Kingdom’s transformation into a global leader in urban development excellence. The success of this vision will ultimately depend on the commitment of all stakeholders to work collaboratively, think boldly, and execute diligently. A key takeaway is that long-term success in PPPs requires meticulous feasibility studies, transparent communication and stable leadership, along with secure and diversified funding sources. Moreover, maintaining regulatory clarity and adaptable project management structures is essential for mitigating risks and ensuring sustainable growth, especially for giga-projects with significant global investor involvement.

As Saudi Arabia continues its journey toward Vision 2030 and beyond, PPPs will undoubtedly stand as one of the most powerful instruments in its development toolkit—bridging resources, capabilities, and aspirations to create lasting value for generations to come.

Leave a Reply